Nepal’s OTC Market

For most Nepali investors, the stock market begins and ends with the Nepal Stock Exchange (NEPSE). The general belief is simple: if a company is not listed on NEPSE, its shares cannot be bought or sold. Yet, behind this commonly accepted view exists a lesser-known but legally recognized marketplace that quietly facilitates the trading of shares of non-listed public companies, the Over-the-Counter (OTC) market. Over the years, shares of prominent enterprises such as Ncell, WorldLink, Fonepay, IME Digital Solutions, Kathmandu Medical College and even NEPSE itself have changed hands through this platform, often at prices that surprise traditional stock market participants.

The OTC market, as its name suggests, refers to a system of trading that takes place outside the conventional automated stock exchange. Unlike NEPSE, where transactions occur electronically through brokers using the Trading Management System (TMS), OTC trading is conducted through a separate counter operated by NEPSE. Transactions are executed based on mutual agreement between buyers and sellers, supported by documentation and regulatory oversight, but without real-time electronic matching. Internationally, OTC markets are commonly used to trade bonds, derivatives, and other specialized financial instruments. In Nepal, however, the OTC market primarily serves as a platform for trading shares of public limited companies that are not listed on NEPSE or have been delisted.

The distinction between NEPSE and the OTC market is fundamental. NEPSE is a fully automated, highly regulated exchange where only companies that have received approval from the Securities Board of Nepal (SEBON) and issued an Initial Public Offering (IPO) can be listed. Prices are discovered through continuous auction, and settlement is handled by the Central Depository System and Clearing Limited (CDSC). The OTC market, on the other hand, does not host listed companies. It exists specifically to accommodate public companies that are outside the formal exchange framework, while still providing a legal mechanism for share transfers.

Companies eligible for OTC trading in Nepal fall into three broad categories. The first category consists of non-listed public limited companies. These are firms that are registered as public companies with the Office of the Company Registrar but have not yet been listed on NEPSE. Many of them intend to issue IPOs in the future, while others remain unlisted due to strategic or compliance reasons. Well-known examples include WorldLink, Fonepay, IME Digital Solutions, Jagadamba Spinning Mills, Kathmandu Medical College, Alpha Capital and Shree Distillery. It is important to note that private limited companies are strictly prohibited from OTC trading because their shares are not open to the general public.

The second category includes delisted public limited companies. These firms were once listed on NEPSE but were removed after failing to comply with regulatory requirements, such as submitting financial statements on time, holding annual general meetings, or maintaining minimum operational standards. Delisting does not eliminate shareholder ownership. Thousands of investors may still hold shares of such companies, and the OTC market offers them a secondary platform to buy or sell those holdings.

The third group comprises pre-IPO public companies. These are companies that are in the process of preparing for public issuance but have not yet been listed. In some cases, existing shareholders or promoters wish to transfer their shares before the IPO, and OTC provides a legal avenue for such transactions. Examples include Hotel Forest Inn, Kantipur Television, Annapurna Cable Car and Laxmi Steels.

The importance of Nepal’s OTC market lies in its ability to provide liquidity where none would otherwise exist. Without OTC, shares of unlisted or delisted public companies would be virtually illiquid, trapping investors in long-term positions with no exit route. The market also supports companies transitioning toward IPO by establishing early price discovery and enabling share transfers. In this sense, OTC functions as a bridge between the private corporate world and the formal capital market.

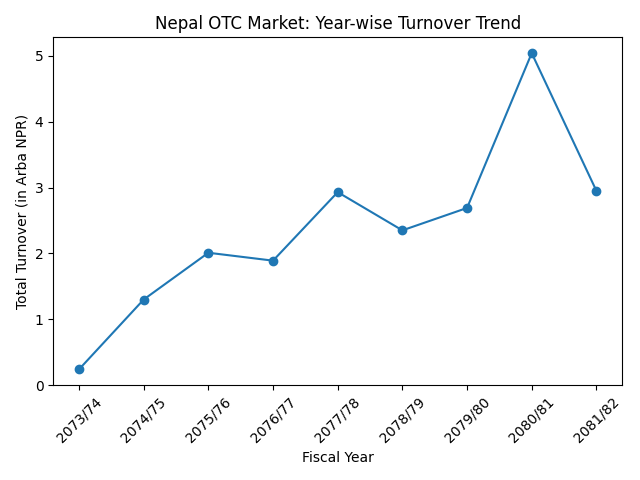

Nepal introduced the OTC Market Regulations in 2065 B.S., and formal OTC trading began in 2015 A.D. Since then, approximately 244 companies have participated in OTC transactions. Trading takes place on working days between 11:00 AM and 1:00 PM at the NEPSE office in Kathmandu. Although discussions have been held about digitizing OTC operations, the system remains largely physical and manual.

Source: Nepal Stock Exchange

The trading process in the OTC market follows a structured but paperwork-intensive procedure. A seller must first submit a sell order form, which must be verified by the issuing company whose shares are being sold. This sell order remains valid for ninety days. Once registered at the OTC counter, potential buyers can submit buy order forms along with at least ten percent of the total transaction value as a deposit. Company name, quantity, and quoted price are displayed on the OTC price board. When a matching order is found, or when both parties reach mutual agreement, the transaction moves toward settlement.

Following agreement, sellers submit legally prescribed documents for share transfer, while buyers deposit the remaining payment along with transfer fees and applicable charges. Under Nepal’s tax law, individuals are required to pay ten percent capital gains tax, domestic institutions fifteen percent, and foreign investors twenty-five percent. After verification and clearance by NEPSE, payment is released to the seller within approximately five working days, and ownership is formally transferred to the buyer.

Pricing in the OTC market is based on negotiation rather than continuous auction. However, NEPSE has established a safeguard whereby OTC share prices cannot be lower than the company’s per-share net worth. This rule aims to reduce undervaluation and tax evasion, though it cannot eliminate such risks entirely. Compared to NEPSE, OTC remains less transparent, with limited publicly available data on historical prices and volumes.

The OTC market offers distinct advantages. It allows investors to gain exposure to promising companies long before an IPO. It provides an entry point into well-known brands that remain unlisted. It also presents opportunities to acquire undervalued shares of delisted companies that may later recover or relist. For patient, long-term investors with strong research capability, OTC can deliver substantial returns.

At the same time, the risks are considerable. Liquidity is low, meaning it can be difficult to find buyers or sellers. Financial information may be limited or outdated. Price manipulation and rumor-driven valuation are more likely than in the regular market. Settlement takes longer, and regulatory protection is comparatively weaker.

Nepal’s OTC market, therefore, is not a playground for short-term traders. It is a niche segment designed for informed investors who understand corporate fundamentals and are willing to accept higher uncertainty in exchange for potential long-term reward.

In conclusion, the OTC market represents a hidden but essential layer of Nepal’s capital market architecture. It connects unlisted public companies, early-stage firms, delisted entities and investors under a legally recognized framework. While imperfect and underdeveloped, it plays a crucial role in expanding market depth and financial inclusion. For those who approach it with discipline and due diligence, the OTC market can serve as a gateway to opportunities that remain invisible on NEPSE’s trading screen.